Crowdfunding hands entrepreneurs something rare: a mass-produced market experiment that

returns both a verdict (the goal is reached or not) and a continuous measure of demand (how much was raised).

Studying 9,322 Kickstarter creators surveyed about motives, beliefs, and post-campaign choices and matched to

platform records, we document a double dissociation in how founders process this information.

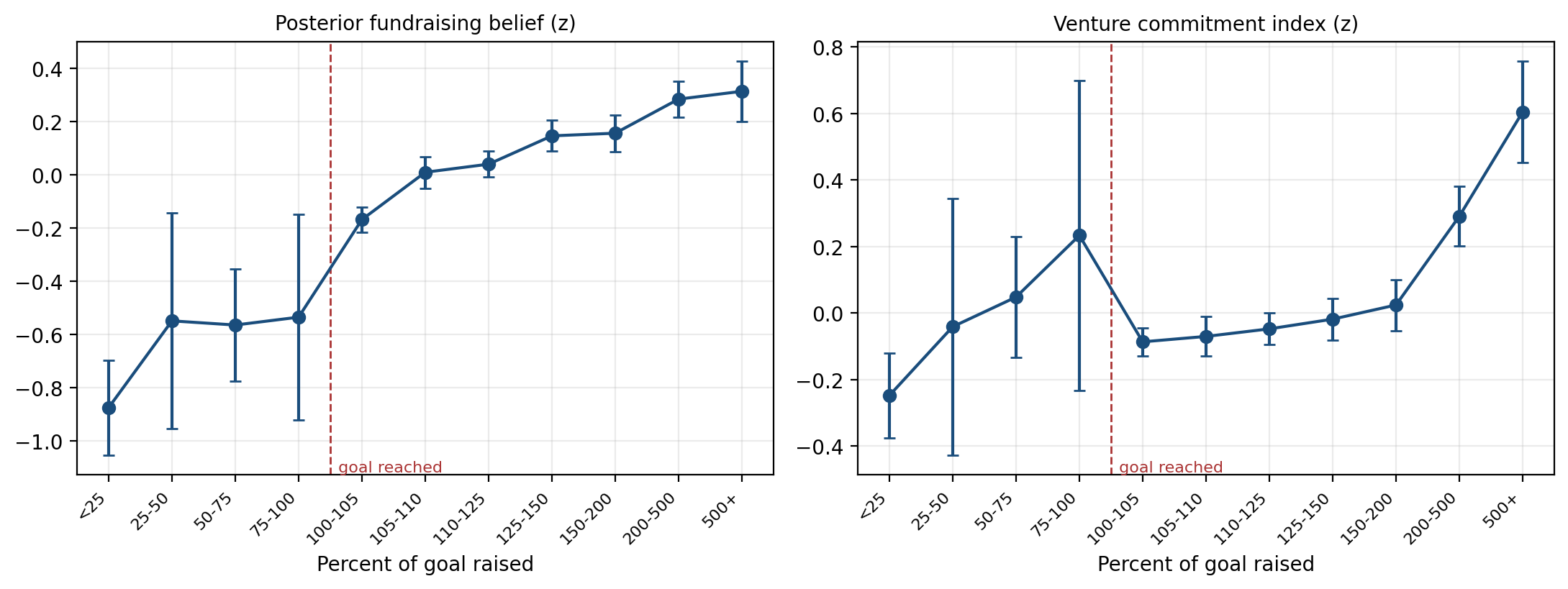

Posterior beliefs about market demand are purely reference-dependent: holding dollars raised constant, they

track only performance relative to the founder's self-chosen goal — jumping at the threshold, responding steeply

for the first ten points past it, and flattening thereafter — while loading negatively on absolute scale. Venture

commitment shows the mirror image: it tracks absolute dollars raised, with zero weight on the goal-relative verdict.

The belief kink is located uniquely at the founder's own goal, replicates with frozen specifications in split

halves and a held-out sample, and is costly: funding magnitude beyond the threshold still predicts realized

revenue and earnings. The verdict-reading is universal — in pre-registered tests, creators who launched explicitly

"to see if there was demand" (39%) update no more elastically than others. Founders' minds read the verdict;

their ventures follow the money; and the evidence in between goes largely unused.